The Opening: Brand and Mission

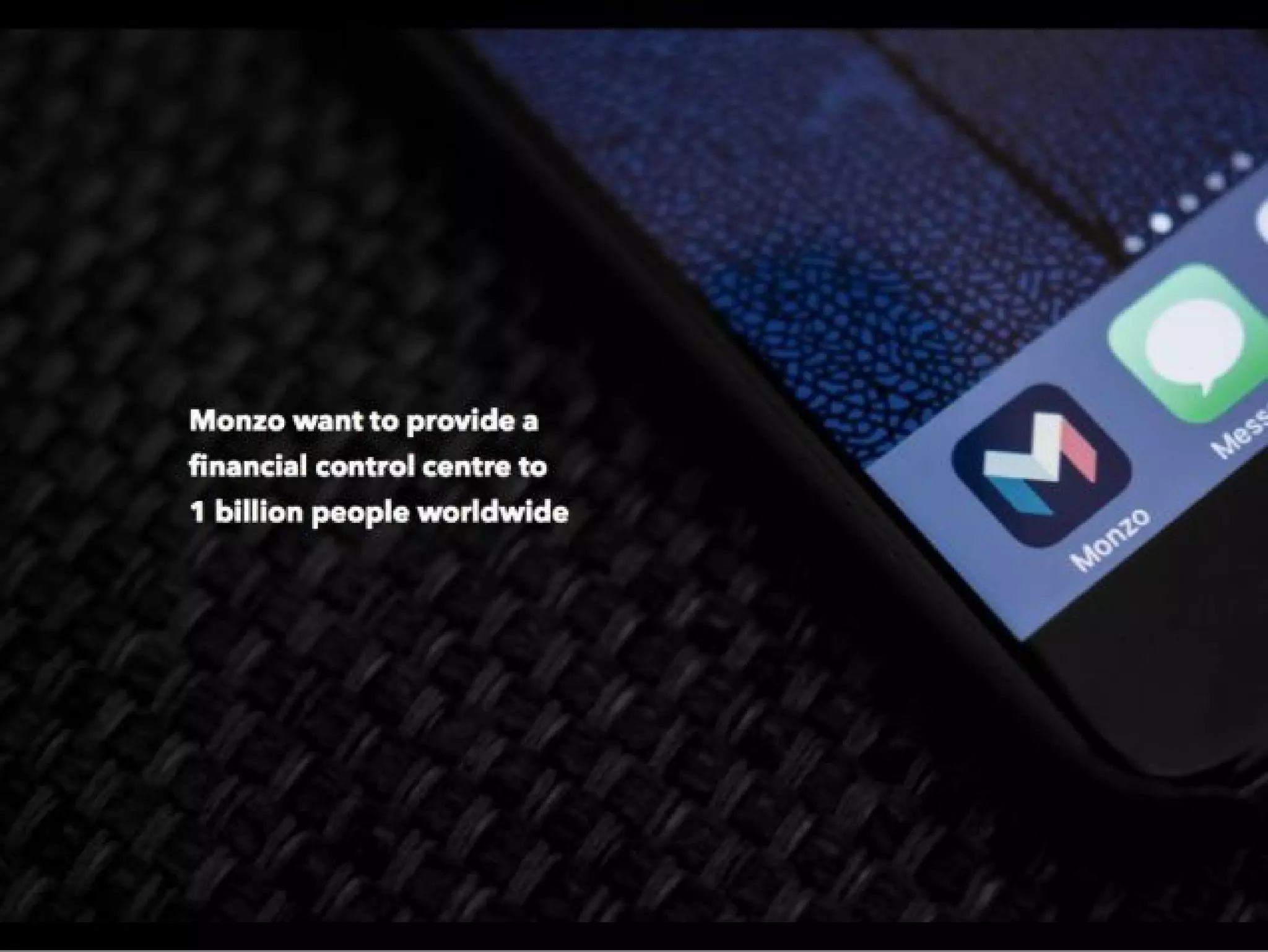

Slide 1 (cover) and slide 2 set a strong emotional and mission-driven tone: they open with the Monzo brand and a bold ambition — to provide a financial control centre to 1 billion people worldwide. The visuals (celebratory crowd, app icon) and short declarative copy establish identity and aspiration immediately, making it easy for investors to understand what Monzo aims to become beyond a single product. This is effective because it leads with vision rather than detail, which helps frame the rest of the deck as steps toward that outcome.

Founders can learn the value of starting with a concise mission and strong branding. It orients the audience and primes investors to interpret traction and technical claims as progress toward a large, relatable goal. Use a simple, high-level ambition early to give later metrics context and to make the story cohesive.